Fintech leaders face constant pressure to protect customer data while scaling fast. Meeting SOC 2 audit requirements for fintech companies solves that problem by proving your systems are secure and reliable—building trust with partners, regulators, and customers.

What are SOC 2 audit requirements for fintech companies?

SOC 2 is a security framework focused on how organizations manage customer data. For fintech companies, SOC 2 audit requirements define the controls and processes needed to demonstrate strong security, availability, processing integrity, confidentiality, and privacy.

What it is

SOC 2 is an attestation standard created by the AICPA that evaluates service organizations on Trust Services Criteria (TSC). Fintech firms typically pursue a Type II report, which tests controls over time—not just design.

Why it matters for fintech

Fintech companies handle sensitive financial and personal data. A SOC 2 report shows stakeholders you follow best practices, reduces vendor friction, and helps meet regulatory expectations.

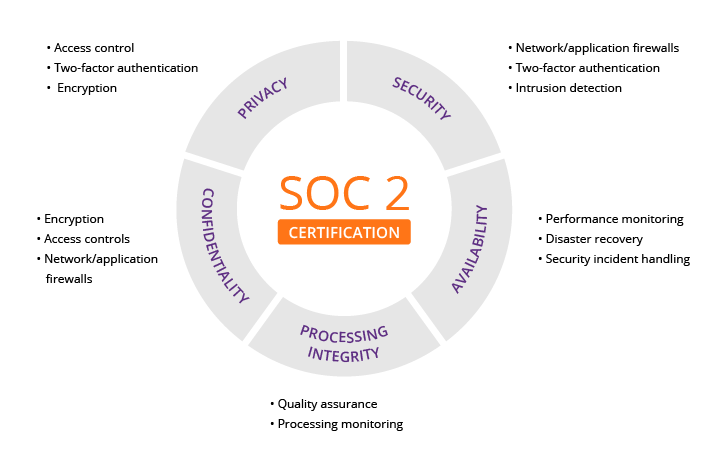

Core SOC 2 components and fintech-focused controls

Understanding the core components helps prioritize work. SOC 2 centers on five Trust Services Criteria. Fintechs often emphasize security, confidentiality, and privacy.

Key criteria explained

- Security: Protect systems against unauthorized access.

- Availability: Ensure systems are available to meet commitments.

- Processing Integrity: Ensure transactions are complete and accurate.

- Confidentiality: Protect sensitive fintech data like account numbers.

- Privacy: Protect personal data collection and use.

Common fintech controls and strategies

Controls translate to practical actions. Typical fintech controls include:

- Access controls: Role-based access, MFA, privileged access monitoring.

- Encryption: Data at rest and in transit.

- Change management: Documented change approvals and testing.

- Incident response: Playbooks, alerting, and post-incident reviews.

- Vendor management: Due diligence, contracts, and monitoring.

- Logging and monitoring: Centralized logs, SIEM, and alerting thresholds.

Tools, platforms and automation

Use tools to reduce manual work and improve control evidence. Fintech companies often combine security tooling, governance platforms, and automated evidence collection.

Recommended tool categories

- Identity & Access Management (IAM): Okta, Azure AD, or similar.

- Encryption and key management: Cloud KMS, Hardware Security Modules.

- SIEM & monitoring: Splunk, Datadog, or cloud-native options.

- GRC and audit automation: Compliance platforms that map controls to evidence.

- Vulnerability scanning: Automated scanning and patch tracking.

Automation speeds audits, reduces human error, and keeps logs ready for reviewers.

Benefits of achieving SOC 2

- Builds customer and partner trust quickly.

- Reduces sales friction and speeds contracting.

- Demonstrates regulatory awareness and diligence.

- Identifies security gaps proactively.

- Makes risk management repeatable and measurable.

Comparison: SOC 2 vs alternatives for fintech

| Standard | Focus | Best for | Typical outcome |

|---|---|---|---|

| SOC 2 | Operational controls (security, availability, confidentiality, privacy) | Cloud-native fintech platforms, SaaS payments, data processors | Attestation report (Type I or II) |

| PCI DSS | Cardholder data security | Payment processors, merchants handling card data | Compliance certificate and report |

| ISO 27001 | Information security management system (ISMS) | Enterprises seeking internationally recognized ISMS | Certification by accredited body |

| HIPAA | Protected health information | Fintechs dealing with health-related financial data | Compliance through controls and audits |

Which to choose?

Fintech companies that handle sensitive financial data and serve business customers often prioritize SOC 2. PCI DSS is mandatory when card data is in scope. Many companies combine frameworks for full coverage.

How to prepare: Practical roadmap

Preparation reduces audit time and cost. Follow a pragmatic roadmap:

- Scoping: Define services, systems, and data in scope.

- Gap assessment: Map current controls to SOC 2 criteria.

- Remediation: Fix gaps and document procedures.

- Evidence collection: Centralize logs, configs, and policy artifacts.

- Pre-audit testing: Run internal reviews or engage a readiness assessor.

- Formal audit: Schedule and complete the SOC 2 Type II audit period.

Expert insight

Security leaders often say: start with clear scoping and evidence pipelines. Automate log retention, IAM workflows, and change control to make the auditor’s job straightforward. Treat SOC 2 as continuous improvement, not a one-time checklist.

Use cases: How fintechs benefit in real scenarios

Onboarding enterprise clients

Large banks or B2B customers frequently require SOC 2. Presenting a Type II report accelerates procurement and contract negotiations.

Raising funding or entering partnerships

Investors and partners look for operational maturity. A SOC 2 report is a trust signal during due diligence.

Expanding to regulated markets

SOC 2 helps demonstrate baseline controls when entering new regulatory jurisdictions or integrating with financial institutions.

Frequently Asked Questions

1. How long does a SOC 2 Type II audit take?

Typical timelines are 3–12 months for the audit period plus 4–8 weeks for report preparation. Preparation time varies based on how mature your controls are.

2. What’s the difference between Type I and Type II?

Type I evaluates control design at a specific point in time. Type II evaluates operating effectiveness over a period (usually 3–12 months). Fintechs usually pursue Type II for customer confidence.

3. Which Trust Services Criteria should fintechs prioritize?

Security is required and should be the priority. Confidentiality and privacy are often critical for fintechs. Availability and processing integrity matter if you provide transactional services.

4. Can small fintech startups afford SOC 2?

Yes. Startups can scope narrowly, use shared cloud services, and automate evidence to control costs. A phased approach—starting with internal readiness—reduces the financial burden.

5. Do I need a consultant to pass SOC 2?

Not strictly, but many teams hire readiness assessors to speed preparation and avoid common pitfalls. Consultants can help scope, document controls, and build evidence pipelines.

Conclusion and next steps

Meeting SOC 2 audit requirements for fintech companies is a practical way to prove security and win trust. Start by scoping your in-scope systems, running a gap assessment, and automating evidence collection. Treat controls as products that evolve with your business.

Ready to get started? Map your scope, run a readiness check, and prioritize automation to make the audit process smooth and repeatable.

Fintech Video Marketing Strategies That Drive Engagement , Fintech Social Media Strategies for Brand Growth , Fintech Copywriting Tips to Improve Conversions and Trust

Leave a Reply