How Fintechs with Advanced Fraud Prevention stand apart from Competitors is more than a marketing claim — it defines market leadership. In a world of digital payments, identity theft, and regulatory pressure, fintechs that invest in proactive, intelligent fraud prevention systems deliver safer services, higher trust, and measurable business advantage.

What it is: defining advanced fraud prevention in fintech

Advanced fraud prevention combines machine learning, behavioral analytics, real-time monitoring, identity verification, and adaptive rules to detect and stop fraud before it impacts customers or the business. It moves beyond static rules to contextual decisions that consider device signals, transaction patterns, and risk scoring.

Core components of advanced fraud prevention

Fraud detection engines use supervised and unsupervised learning to spot anomalies. Identity verification (KYC) verifies users during onboarding. AML screening checks for suspicious transaction flows. Behavioral biometrics analyzes how a user types, swipes, or navigates to detect account takeover attempts.

Why data and orchestration matter

Data enrichment, shared fraud intelligence, and orchestration layers let fintechs correlate signals across channels. This layered approach reduces false positives and enables efficient investigations.

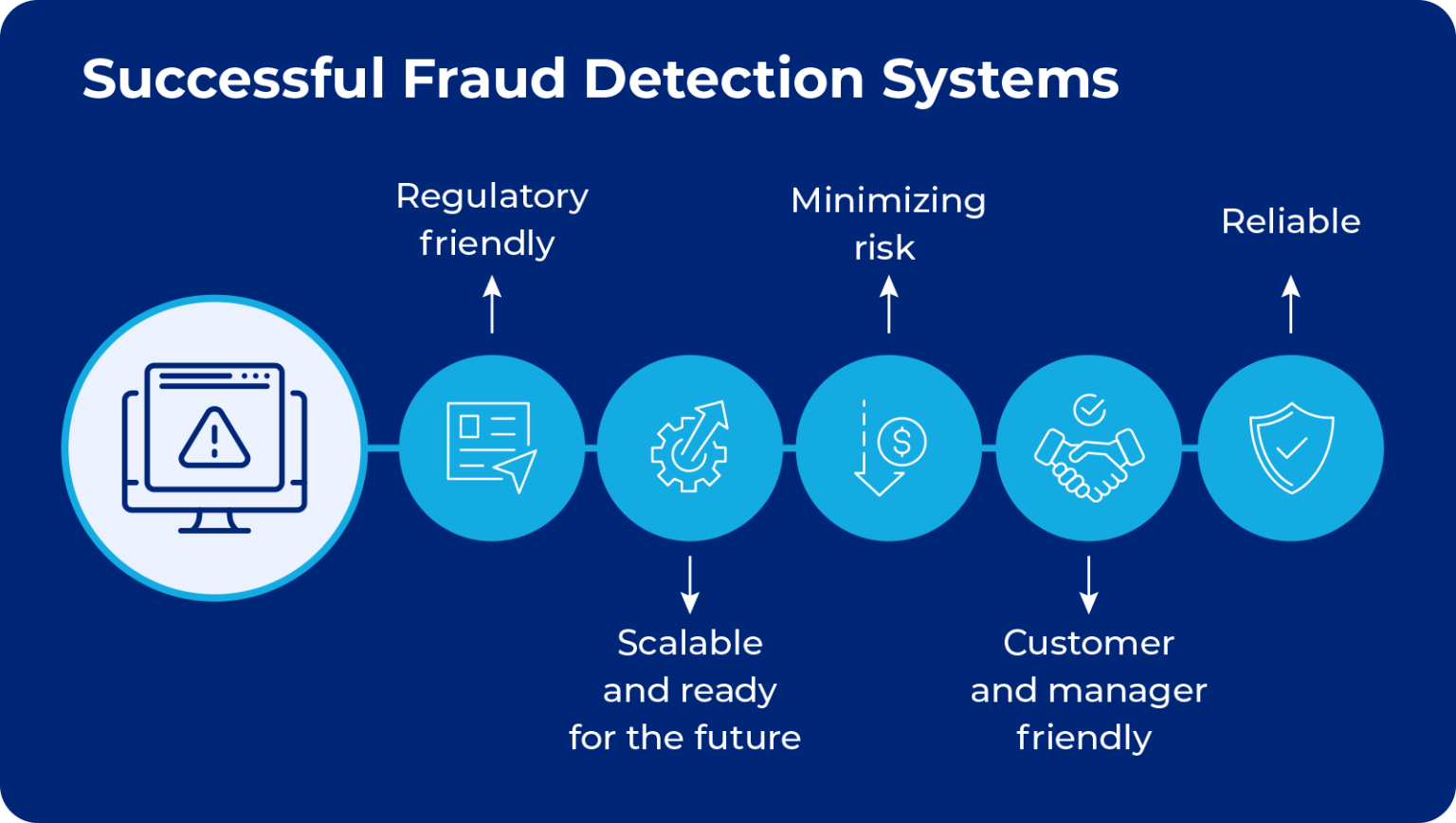

Why it matters: Business, Compliance, and Customer trust

How Fintechs with Advanced Fraud Prevention stand apart from Competitors because they protect revenue, reduce operational costs, and build trust. Fraud has direct costs (chargebacks, losses) and indirect costs (customer churn, reputational damage).

Regulatory compliance and risk reduction

Robust prevention helps meet KYC/AML obligations and demonstrates a strong control environment to regulators and partners. This reduces fines and speeds up approval for new services.

Customer experience and retention

When fraud prevention is accurate and frictionless, customers enjoy fast onboarding and secure transactions, improving retention and lifetime value.

Features / Services / tools offered by leading fintechs

Leading fintechs integrate multiple specialized tools to stay ahead of threats and competitors.

Real-time transaction monitoring

Continuous scoring of transactions with configurable thresholds and automated actions such as hold, challenge, or approve.

Adaptive machine learning models

Models that retrain on fresh data and detect evolving attack patterns without manual rule updates.

Behavioral biometrics and device intelligence

Silent authentication techniques that identify suspicious behavior without interrupting legitimate users.

Identity verification and document authentication

Biometric matching, liveness checks, and automated document verification to reduce fake accounts.

Consortium/Shared intelligence feeds

Threat feeds and anonymized sharing across partners to surface emerging fraud trends quickly.

Orchestration and case management

Automated workflows, analyst tools, and a single view of risk to close incidents faster.

Benefits: why businesses choose advanced prevention

- Lower fraud losses and chargebacks

- Faster onboarding with reduced friction

- Improved approval rates and fewer false declines

- Regulatory compliance and audit readiness

- Stronger brand trust and customer loyalty

- Operational efficiency through automation

Comparison: fintechs with advanced fraud prevention vs typical competitors

| Capability | Fintechs with Advanced Fraud Prevention | Typical Competitors |

|---|---|---|

| Detection approach | Adaptive ML + behavioral analytics | Rule-based and manual review |

| False positive rate | Low due to contextual scoring | Higher, causing customer friction |

| Onboarding friction | Low with seamless verification | Higher, more manual checks |

| Operational cost | Lower per incident via automation | Higher due to manual investigations |

| Regulatory readiness | Proactive reporting and controls | Reactive, often ad hoc |

| Speed to detect new threats | Fast via shared intelligence | Slow, reliant on incidents |

Expert insight

Industry experts agree that prevention wins over remediation. According to senior security leaders, integrating identity, device, and behavioral signals into a unified risk engine reduces both fraud and friction. Strategic investments in data quality and automation are decisive differentiators for fintechs seeking scale.

Practical guidance from practitioners

Start small with API-based services, tune models with your own data, and prioritize signals that reduce false declines. Build feedback loops between fraud analysts and model teams to refine detection in production.

Use cases: where advanced fraud prevention makes the biggest impact

Payments and card issuing

Prevent stolen-card transactions, synthetic identity fraud, and merchant collusion by combining real-time scoring and device intelligence.

Digital onboarding and lending

Reduce loan fraud and onboarding fraud using document verification, KYC, and behavioral profiling.

Account takeover and credential stuffing

Detect abnormal session patterns, velocity spikes, and impossible travel signals to block takeovers before damage occurs.

Cross-border transactions and remittances

AML rules augmented with transaction profiling and peer-group analysis to flag sophisticated laundering attempts.

Pricing / Cost overview

Pricing models vary. Most providers offer tiered subscription plans, pay-per-transaction, or hybrid pricing with setup fees. Expect costs to reflect the depth of features:

- Basic: rule-based monitoring, limited API calls — lower monthly fee

- Standard: ML scoring, identity checks, moderate transaction volume

- Premium: full orchestration, behavioral biometrics, consortium feeds, priority support

Investing in advanced prevention often yields a positive ROI through reduced chargebacks and operational savings. Request a pilot or proof of concept to measure impact on your own metrics.

FAQs

1: Will this slow down my customers?

No. Properly implemented systems use silent signals and risk-based authentication to minimize friction. Only high-risk flows trigger stronger checks.

2: Can small fintechs afford these tools?

Yes. Modern solutions are modular and API-driven. Small firms can start with identity verification and transaction scoring, then scale to advanced modules as needed.

3: How do these systems reduce false positives?

By combining multiple signals and using supervised learning tuned on real outcomes, systems distinguish fraud from legitimate unusual behavior and lower false declines.

4: How long to deploy?

Basic integrations can be live in days. Full production deployments with custom models and orchestration typically take weeks to a few months, depending on complexity.

5: How do I measure success?

Track metrics such as fraud loss rate, false positive rate, approval rate, chargebacks, investigation time, and customer satisfaction. A reduction in fraud losses and operational cost indicates success.

Conclusion + CTA

How Fintechs with Advanced Fraud Prevention stand apart from Competitors is clear: they protect customers, lower costs, and accelerate growth. For fintechs aiming to lead, investing in adaptive, data-driven fraud prevention is not optional it is strategic.

If you want to evaluate solutions or run a targeted pilot, start with a risk assessment and a short proof of concept. Contact our team to map a tailored roadmap and begin reducing fraud while improving customer experience.

Fintech Companies DORA Compliance Case Studies: Real Examples & Lessons (2026) , Comparing Unstructured Data Parsing APIs for Fintech Onboarding (2026 Guide) , Top VPN Detection Services for Fraud Prevention Fintech Platforms (2026)

Leave a Reply