Verifying customers across borders is slow, risky, and often costly—but the right tools can make onboarding secure, fast, and compliant worldwide. In this article you’ll learn how modern tools for fintechs to verify user identities across countries reduce fraud, speed revenue, and keep regulators happy.

What “tools for fintechs to verify user identities across countries” mean and why they matter

At its core, this phrase refers to platforms, services, and techniques fintech companies use to confirm who a user is when they sign up or transact across different jurisdictions. These tools combine document checks, biometric verification, database lookups, and compliance workflows so that a fintech can trust a user’s identity no matter where they are located.

Why identity verification matters for fintechs

Cross-border identity verification is essential because fintechs operate where identity rules, data sources, and risk levels vary. Without the right tools fintechs face higher fraud, failed payments, regulatory fines, and poor customer experience. Proper verification protects business reputation and unlocks global growth.

Key features, tools, and strategies

Effective identity verification stacks mix technology, data, and process. Below are the most important components fintechs should consider.

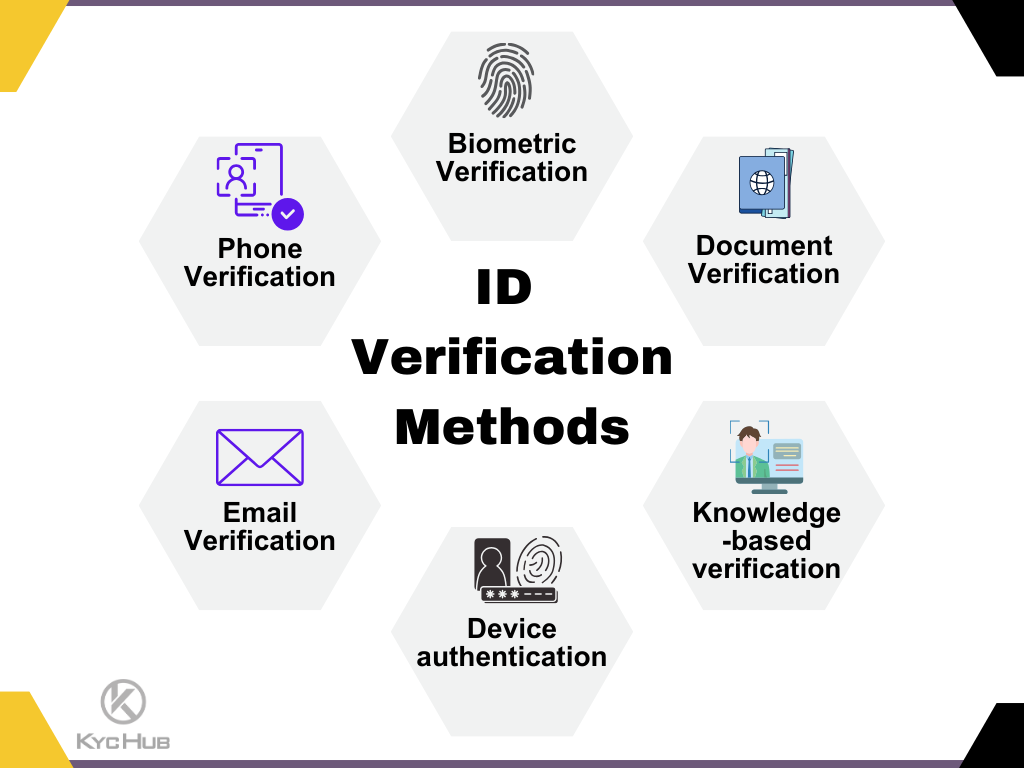

Core verification features

- Document verification: Automated checks on passports, IDs, and driving licenses for authenticity.

- Biometric liveness checks: Face match and anti-spoofing to ensure the person presenting the ID is real and present.

- Global watchlists and sanctions screening: Real-time screening against OFAC, UN, PEP and local lists.

- AML transaction monitoring integration: Linking identity results to transaction risk rules.

- Digital identity or eID support: Connecting to national eID systems where available.

- Data enrichment and ID attribution: Address, phone, and device intelligence to increase confidence scores.

- Localized workflows: Country-specific checks and languages to reduce friction.

- APIs and SDKs: For embedding verification into apps and webflows.

Popular tool types

- Identity verification platforms (IDV) that combine document check, biometrics, and watchlist screening.

- Specialized biometric vendors for face recognition and liveness detection.

- Global AML/ sanctions screening providers.

- Data providers for address, phone, and credit signals by country.

- Open banking and eID connectors for instant bank data or government-backed identity validation.

Benefits of using the right cross-border identity tools

Choosing the right mix of tools delivers clear business outcomes.

- Faster customer onboarding and higher conversion rates

- Reduced fraud losses and chargebacks

- Regulatory compliance with multi-jurisdiction rules

- Improved customer trust and lower churn

- Operational efficiency with automated decisioning

Comparison: Common identity verification providers and capabilities

| Capability | IDV Platform A | IDV Platform B | Biometric Specialist |

|---|---|---|---|

| Global document coverage | 200+ countries | 120 countries | Limited docs, focuses on biometrics |

| Biometric liveness | Advanced 3D liveness | 2D video liveness | Top-tier face match |

| Sanctions & PEP screening | Built-in global lists | Third-party integration | None |

| eID / Open Banking | Connectors for 25 markets | Limited connectors | None |

| SDKs & API | Mobile + web SDKs | API-first with SDKs | SDK for mobile |

| Pricing model | Per-check + volume discounts | Subscription + per-check | Per-scan |

How to choose

Match vendor strengths to your markets: pick broad document coverage if you target many countries, or a biometric specialist if fraud via synthetic identities is your main threat. Also weigh integration complexity, data residency, and SLA requirements.

Expert insight

Leading identity experts emphasize a layered approach. “No single check is enough globally,” says a former fintech compliance director. “Combine document validation, biometrics, and local data sources, and tune the decision rules by country.” Prioritize modular systems so you can add new regional connectors, and keep humans in the loop for edge cases to reduce false positives.

Use cases

1. Digital bank onboarding across 30 countries

A challenger bank used an IDV platform with eID and open banking connectors to verify users in multiple EU and LATAM markets. Result: 40% faster onboarding and a 25% drop in fraud-related account closures.

2. Cross-border payments provider

A payments fintech integrated biometric liveness and global sanctions screening to meet KYC and AML needs. The layered checks prevented account takeover attacks and ensured compliance with partner banks.

3. Crypto exchange expanding internationally

The exchange implemented device intelligence and KYC monitoring to detect synthetic accounts. This reduced money laundering risk while maintaining high conversion by offering localized verification options.

SOC 2 Compliance for Fintech Companies: Complete Guide , Best SOC 2 Audit Firms Specializing in Fintech , SOC 2 Audit Requirements for Fintech Companies Explained

Frequently Asked Questions

1. What is the fastest way to verify users across countries?

Use a combination of eID or open banking where available, plus an automated IDV platform for documents and biometrics. That blend provides instant checks in supported markets and reliable fallbacks elsewhere.

2. Are biometric checks legal everywhere?

Laws vary. Some countries restrict biometric data processing or require explicit consent and data residency. Always consult local legal counsel and choose vendors that support compliant data handling.

3. How do I handle customers from countries with weak or no ID systems?

Use alternative signals: device intelligence, behavioral analytics, third-party data enrichment, and manual review for higher-risk cases. Consider tiered onboarding with limited access until verification is completed.

4. What are common integration challenges?

Typical problems include inconsistent document formats, latency from third-party services, GDPR or local data residency requirements, and differing watchlist formats. Plan for retries, caching of non-sensitive results, and fallbacks.

5. How much does cross-border verification cost?

Costs vary by coverage and depth. Expect per-check fees for documents and biometrics, plus subscription or connector fees for eID/open banking. Volume discounts and risk-based pricing often apply. Evaluate total cost of ownership including manual review and false positive handling.

Conclusion and next steps

Tools for fintechs to verify user identities across countries are essential to scale globally while reducing fraud and staying compliant. Start by mapping your target markets, identifying the verification gaps, and selecting modular vendors that let you mix document checks, biometrics, and local connectors. Pilot in a few countries, measure conversion and fraud metrics, then expand with tuned decisioning.

Ready to improve onboarding and reduce risk? Start a pilot with a layered ID verification stack and track lift in conversion and fraud reduction.

Call to action: Evaluate one identity platform and one biometric specialist in a 90-day pilot to see immediate ROI.

Leave a Reply