Many small businesses and startups struggle with slow payments, weak security, and poor customer experience. Learning how to create a fintech app can fix those problems and unlock faster payments, better trust, and new revenue streams.

How to create a fintech app: a quick overview

A fintech app is software that helps people manage money, pay, invest, or borrow using mobile or web interfaces. This guide breaks down what a fintech app is, why it matters, the key features and tools, development strategies, and real-world use cases so you can plan and launch with confidence.

What a fintech app is

At its core, a fintech app connects users to financial services. That includes digital wallets, payment processing, lending platforms, investment dashboards, expense tracking, and business banking features. Fintech apps use APIs, encryption, and compliance layers to handle money securely.

Why fintech apps matter

Fintech apps matter because they make financial tasks faster, cheaper, and more accessible. They let businesses accept digital payments, manage cash flow, offer credit, and personalize financial services at scale. For customers, fintech apps provide convenience, transparency, and control.

Key features, tools, and technologies for building fintech apps

When you build a fintech app, choose features and tools that balance user experience, security, and compliance.

Essential features

- Secure user authentication (biometrics, MFA)

- Payments and card processing (PCI-compliant)

- KYC and identity verification

- API integrations with banks and payment processors

- Real-time account balances and transaction histories

- Notifications and alerts

- Analytics and reporting for users and admins

Common tools and tech stack

- Frontend: React Native, Flutter, or web frameworks for cross-platform UI

- Backend: Node.js, Python (Django / Flask), or Java/Kotlin for robust services

- Databases: PostgreSQL or MySQL for relational data; Redis for caching

- Payment processors: Stripe, Adyen, PayPal, or local providers

- Banking APIs: Plaid, TrueLayer, Open Banking connectors

- Identity/KYC: Jumio, Onfido, or built-in verification flows

- Security: TLS, tokenization, rate limiting, vulnerability scanning

- Cloud: AWS, Google Cloud, or Azure for scalability

Strategy tips

- Start with a minimum viable product (MVP) focusing on one core value: payments, lending, or bookkeeping.

- Design for compliance from day one—know your regional banking and data rules.

- Prioritize secure architectures and third-party risk management.

- Use modular APIs so you can swap providers without big rewrites.

Benefits of a fintech app for modern businesses

- Faster payments and reduced processing costs

- Better customer retention through personalized services

- Improved cash flow visibility and forecasting

- New revenue streams from value-added financial services

- Scalable operations with automated workflows

Comparison: Build in-house vs. use fintech platforms vs. white-label

| Approach | Speed to market | Customization | Cost | Control & Compliance |

|---|---|---|---|---|

| Build in-house | Slow | High | High | Full control (requires expertise) |

| Use fintech platforms/APIs | Fast | Medium | Medium | Shared responsibility |

| White-label solution | Very fast | Low | Low–Medium | Limited control |

How to choose

Choose in-house if you need unique features and long-term control. Choose platforms if you need speed and standard financial functions. Choose white-label to launch quickly with predictable costs.

Expert insight

“Start with a narrow use case and build trust through robust security and clear UX,” says a fintech product lead with experience in payments and banking APIs. “Compliance and partnerships often decide success more than product polish in early stages.”

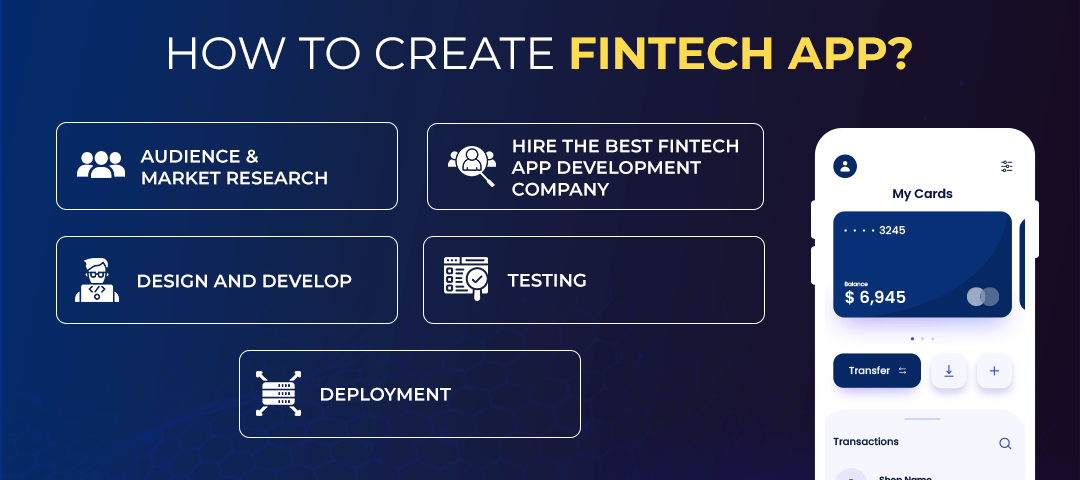

Step-by-step roadmap to develop a fintech app

1. Define the problem and target audience

Decide whether you’re solving payments for SMBs, consumer budgeting, lending, or investing. Narrowing the audience reduces feature bloat.

2. Validate with customers

Run interviews, landing pages, or small pilots to confirm demand and willingness to pay.

3. Choose partners and tech

Select payment processors, KYC vendors, and banking APIs. Pick a stack that supports secure builds and fast iteration.

4. Build an MVP

Implement core flows: onboarding, authentication, core financial action (send money, request payment), and basic reporting.

5. Compliance and security review

Audit code, encrypt sensitive data, and align with PSD2, PCI-DSS, or local regulations. Engage legal counsel if needed.

6. Launch and iterate

Use analytics to track adoption, retention, and fraud signals. Iterate based on user feedback.

Practical use cases

Small business payments

Accept card and bank transfers, reconcile invoices, and automate receipts.

Consumer money management

Help users track budgets, round-ups for savings, and link accounts for a single view of finances.

Embedded lending

Offer credit at checkout or short-term working capital for merchants through underwriting APIs.

Wealth and investment

Provide automated investing, portfolio tracking, or fractional shares for retail customers.

Frequently Asked Questions

1. How much does it cost to create a fintech app?

Costs vary widely. A simple MVP using third-party APIs can start from $50k–$150k. A full-featured, compliant platform built in-house can exceed $500k depending on team and integrations.

2. How long does it take to build a fintech app?

An MVP can take 3–6 months. A production-ready, compliant app typically takes 9–18 months, including legal and security work.

3. What regulations should I consider?

Key regulations include anti-money laundering (AML), know-your-customer (KYC), data protection laws like GDPR, and payment-specific standards such as PCI-DSS. Rules vary by country.

4. Can I use third-party APIs to speed up development?

Yes. APIs for payments, identity verification, and banking data dramatically reduce time to market and help manage compliance burden.

5. How do I keep user data secure?

Use encryption at rest and in transit, strong authentication (MFA), secure key management, regular audits, and follow best practices for secure coding and infrastructure.

Conclusion

How to create a fintech app comes down to solving a clear financial problem, choosing the right partners, and building with security and compliance in mind. Start small, validate quickly, and scale with modular APIs and strong risk controls.

Ready to start building a fintech app that customers trust? Plan your MVP, pick the right integrations, and launch a pilot. How to Build a Fintech App (2026 Beginner Guide) , How Fintech Helps Businesses Improve Cash Flow Management , Best Secure Cloud Hosting Providers for Fintech Startups

Leave a Reply